Springtime Repairs: How to Make DIY Home Maintenance Less Stressful

Springtime repairs around the house can be pretty big chores, eating up your spare time and cutting into your household budget, but they are an important part of keeping your…

Springtime repairs around the house can be pretty big chores, eating up your spare time and cutting into your household budget, but they are an important part of keeping your…

There are always people with too much stuff looking to make some extra money by getting rid of it, and there are always people looking to save a little money…

Sun Mountain Elite Jacket Long known for their well-constructed carry bags and high-tech wheeled carts, Sun Mountain has also made a name for itself as a manufacturer of some of…

Whether it is with the goal of saving money or for the satisfaction of living in the fruits of one’s labors, it has become increasingly popular for homeowners to take…

There are many benefits to homeownership, but one of the top benefits is protecting yourself from rising rents by locking in your housing cost for the life of your mortgage.…

Young people looking to purchase their first home are often put off by the cost involved, including the downpayment and the mortgage process. Fixer-uppers can be a perfectly viable option…

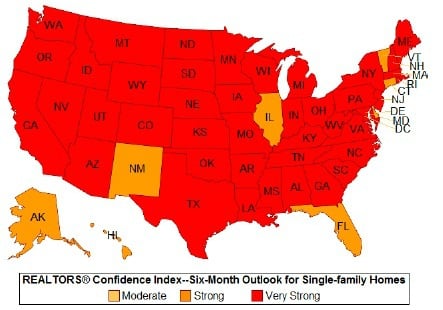

Over the next five years, home prices are expected to appreciate on average by 3.35% per year and to grow by 24.34% cumulatively, according to Pulsenomics’ most recent Home Price Expectation Survey. So,…

So, you’ve decided to sell your house in Naperville. You’ve hired Bill White Homes to help you with the entire process, and Bill White has asked you what level of…

WHY YOU NEED TO SELL THIS SUMMER The market is hot, hot, hot! With interest rates at an all time low for buyers, the market has turned into a feeding…

One of the many benefits of owning your own home is the freedom to find your ‘furever’ friend. By pointing out the aspects of your home that make it ‘pet-friendly’…